East Bay Market Update - December 2025

Monthly Newsletter

Monthly Newsletter

Thinking of buying or selling a home in Berkeley?

At Calia Homes, we specialize in helping East Bay clients navigate the Berkeley real estate market with confidence. Whether you're a first-time buyer searching for the perfect home near the Gourmet Ghetto or a longtime homeowner preparing to sell in the Elmwood or Northbrae neighborhoods, our experienced Berkeley Realtors offer trusted guidance, local expertise, and a people-first approach. With decades of experience and a reputation built on referrals, we’re here to help you make smart, successful real estate decisions in Piedmont and the surrounding East Bay communities.

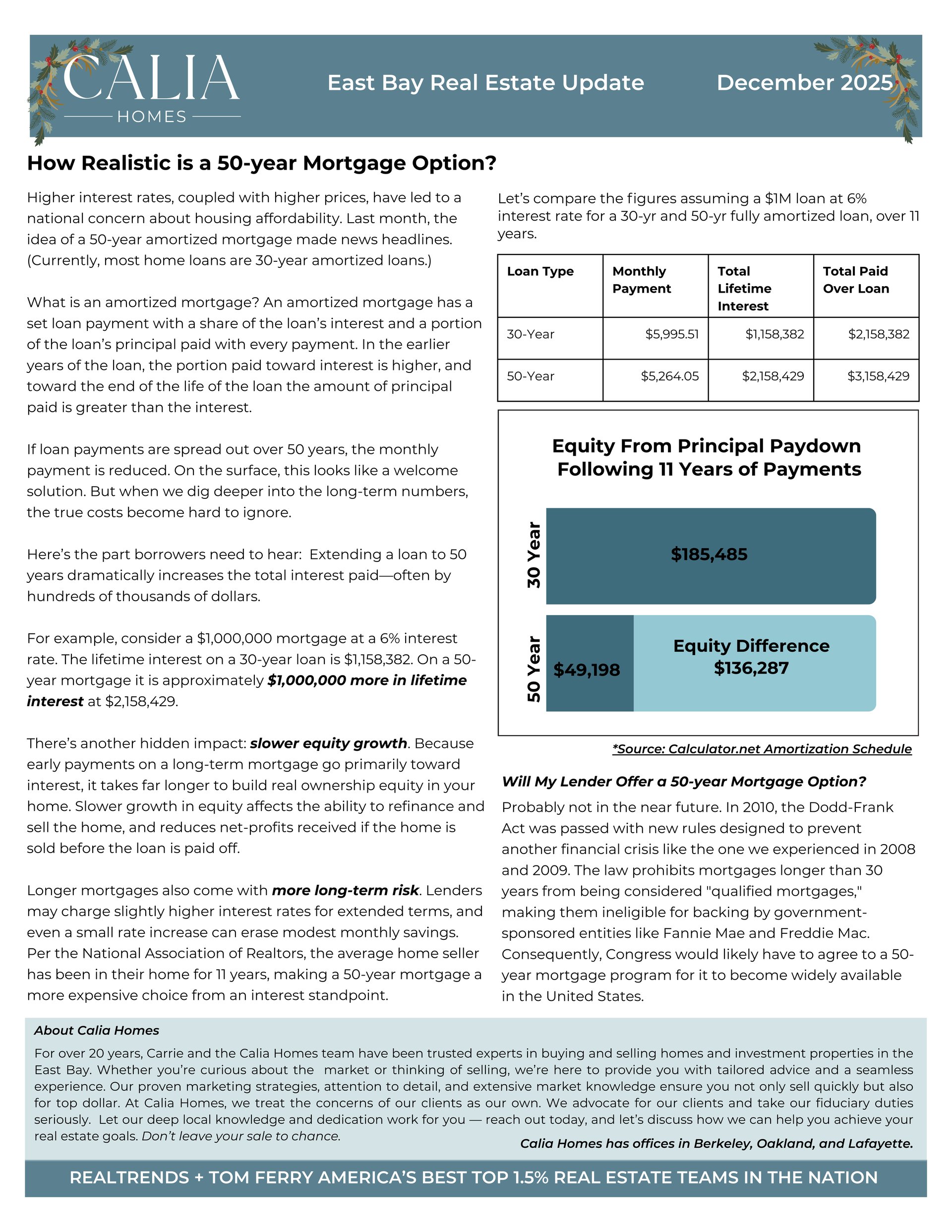

Higher interest rates, coupled with higher prices, have led to a national concern about housing affordability. Last month, the idea of a 50-year amortized mortgage made news headlines. (Currently, most home loans are 30-year amortized loans.) What is an amortized mortgage? An amortized mortgage has a set loan payment with a share of the loan’s interest and a portion of the loan’s principal paid with every payment. In the earlier years of the loan, the portion paid toward interest is higher, and toward the end of the life of the loan the amount of principal paid is greater than the interest. If loan payments are spread out over 50 years, the monthly payment is reduced. On the surface, this looks like a welcome solution. But when we dig deeper into the long-term numbers, the true costs become hard to ignore.

Here’s the part borrowers need to hear: Extending a loan to 50 years dramatically increases the total interest paid—often by hundreds of thousands of dollars. For example, consider a $1,000,000 mortgage at a 6% interest rate. The lifetime interest on a 30-year loan is $1,158,382. On a 50- year mortgage it is approximately $1,000,000 more in lifetime interest at $2,158,429.

There’s another hidden impact: slower equity growth. Because early payments on a long-term mortgage go primarily toward interest, it takes far longer to build real ownership equity in your home. Slower growth in equity affects the ability to refinance and sell the home, and reduces net-profits received if the home is sold before the loan is paid off.

Longer mortgages also come with more long-term risk. Lenders may charge slightly higher interest rates for extended terms, and even a small rate increase can erase modest monthly savings. Per the National Association of Realtors, the average home seller has been in their home for 11 years, making a 50-year mortgage a more expensive choice from an interest standpoint.

Will My Lender Offer a 50-year Mortgage Option?

Probably not in the near future. In 2010, the Dodd-Frank Act was passed with new rules designed to prevent another financial crisis like the one we experienced in 2008 and 2009. The law prohibits mortgages longer than 30 years from being considered "qualified mortgages," making them ineligible for backing by government-sponsored entities like Fannie Mae and Freddie Mac.Consequently, Congress would likely have to agree to a 50-year mortgage program for it to become widely available in the United States.

Stay up to date on the latest real estate trends.

Monthly Newsletter

Monthly Newsletter

At Calia Homes we believe in helping our clients build lasting generational wealth using powerful strategies like the 1031 exchange.

Monthly Newsletter

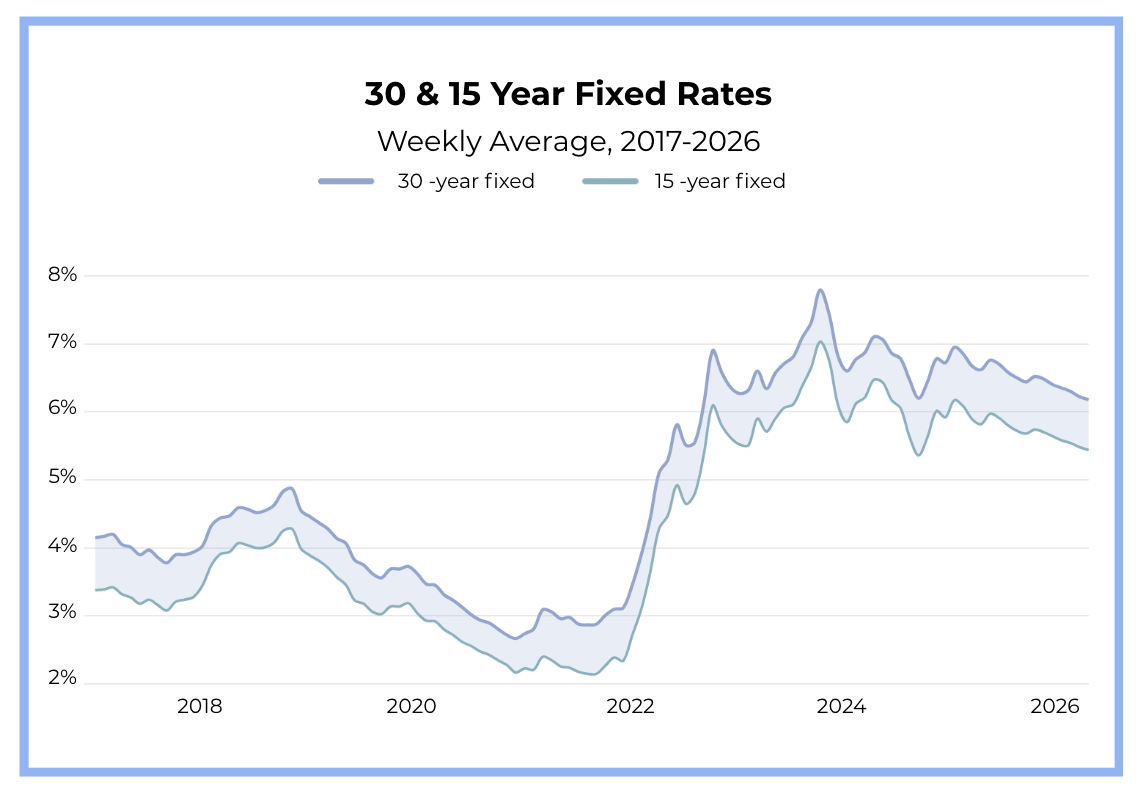

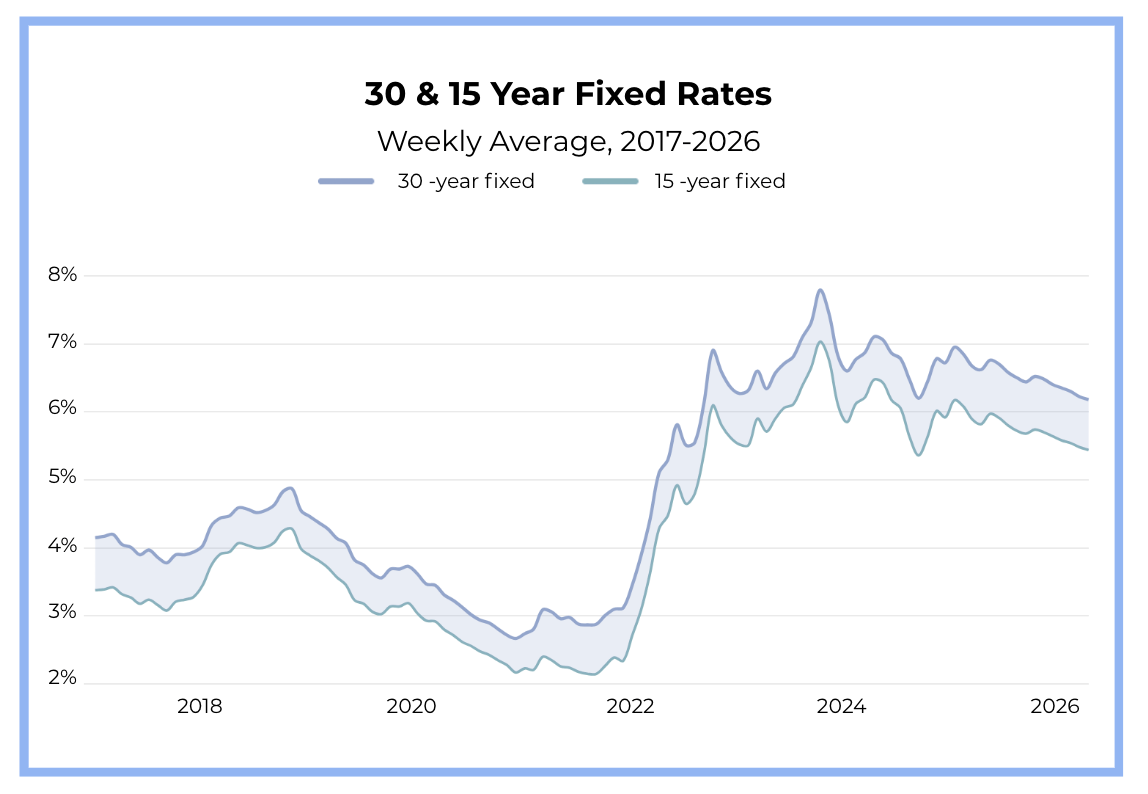

Every spring, clients ask the same question: should I wait for rates to drop? This year, the answer depends less on the Federal Reserve and more on what's happening i… Read more

Monthly Newsletter

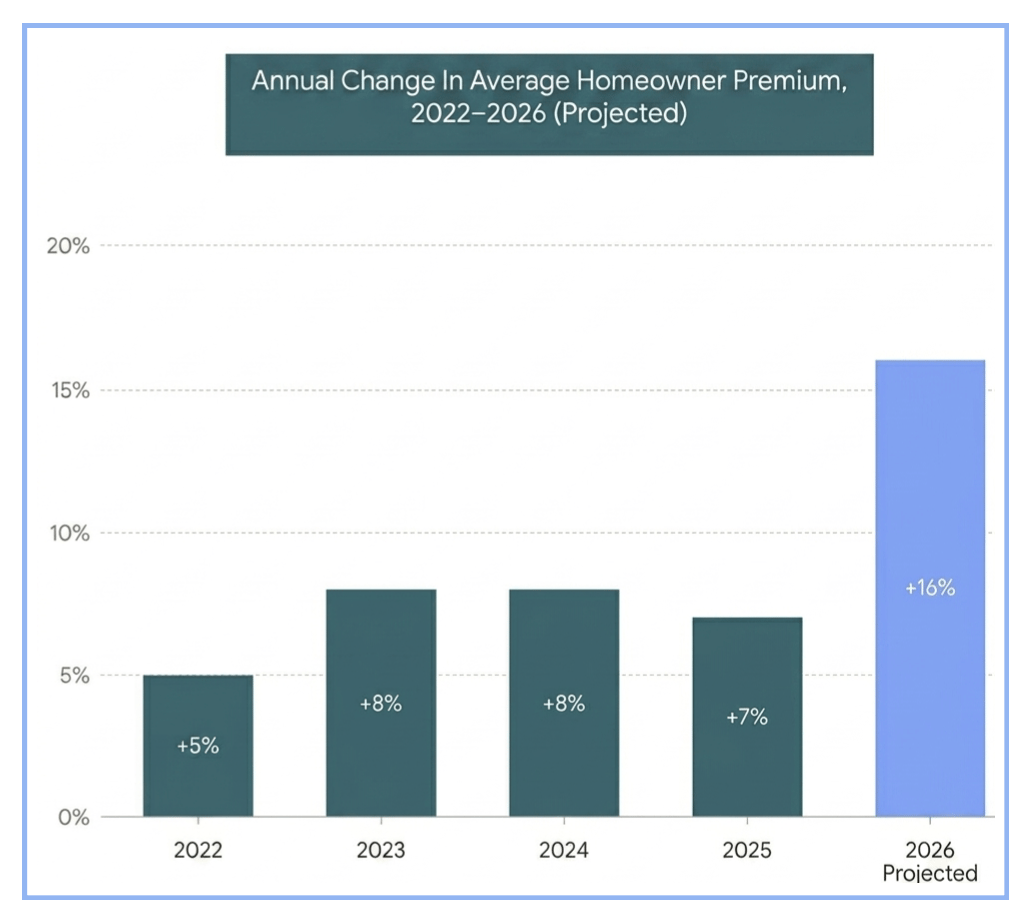

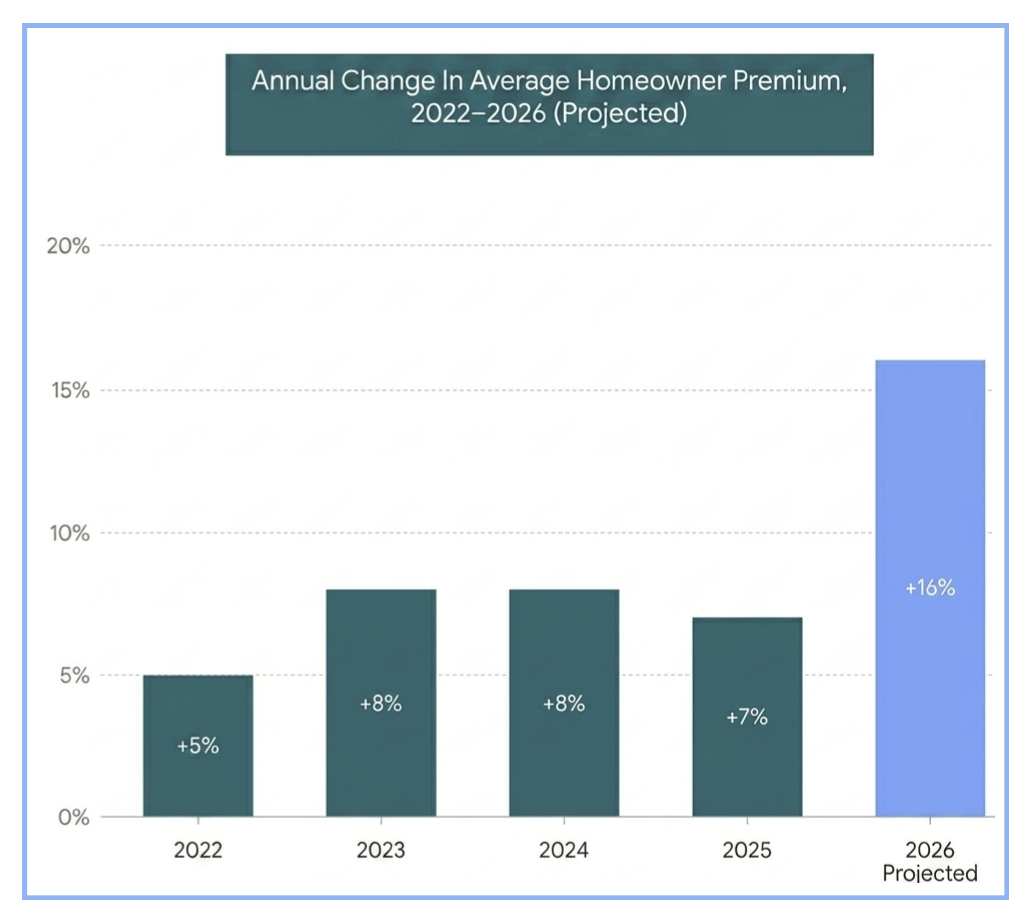

If you’ve opened a renewal notice recently and done a double-take at the premium, you’re not alone.

Monthly Newsletter

Every spring, clients ask the same question: should I wait for rates to drop? This year, the answer depends less on the Federal Reserve and more on what's happening i… Read more

Monthly Newsletter

Every spring, clients ask the same question: should I wait for rates to drop? This year, the answer depends less on the Federal Reserve and more on what's happening i… Read more

Monthly Newsletter

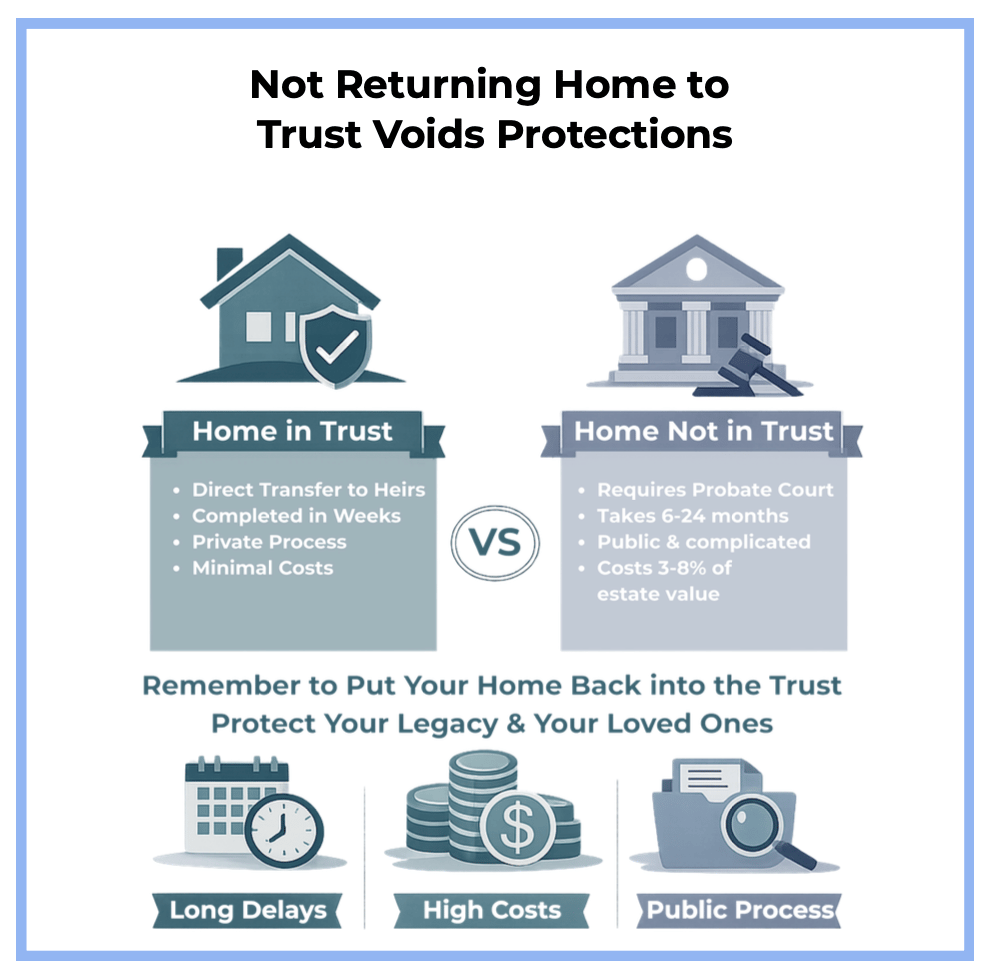

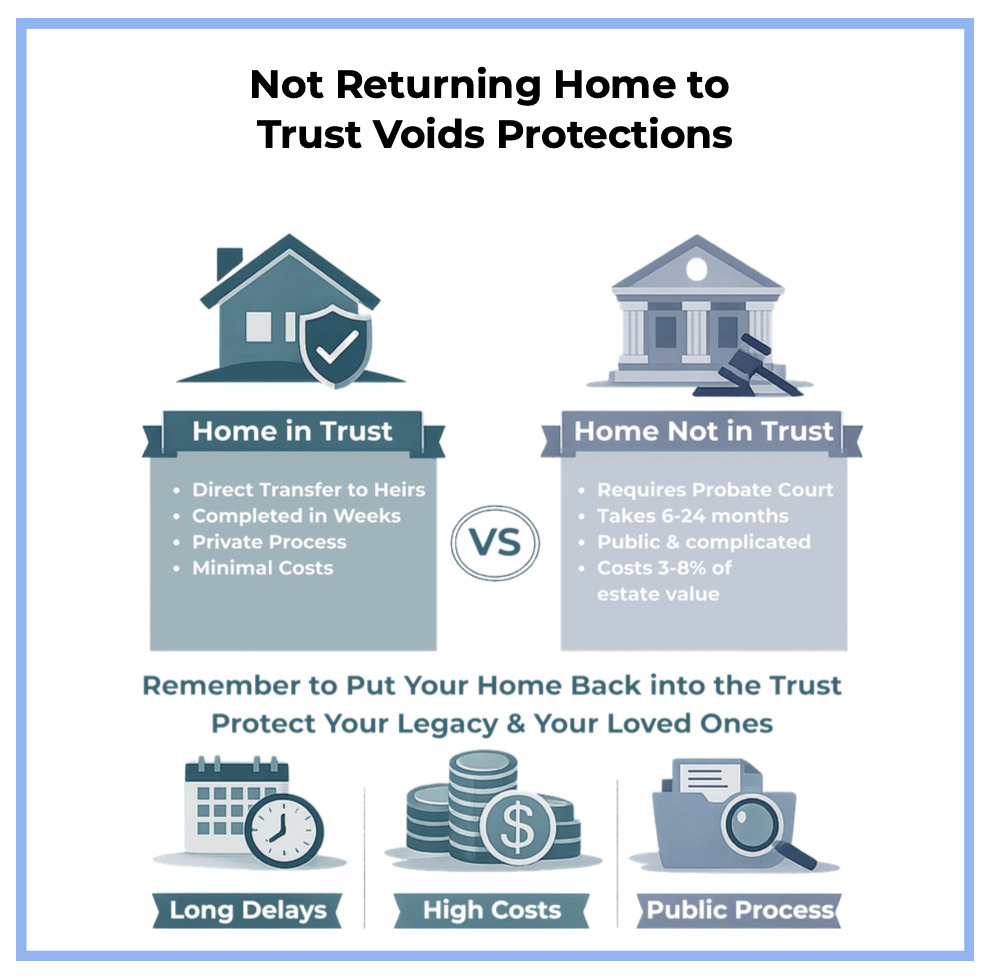

Homeowners often create living trusts for effective estate planning. A trust enables smooth property transfer to loved ones, avoids probate, and keeps family matters p… Read more

Monthly Newsletter

Homeowners often create living trusts for effective estate planning. A trust enables smooth property transfer to loved ones, avoids probate, and keeps family matters p… Read more

Monthly Newsletter

California's newest round of Accessory Dwelling Unit (ADU) laws represents one of the most significant shifts in small-scale housing in years. While...

Let's schedule a time to discuss your goals and aspirations, and determine how we can best help you.